Bank of England stablecoin caps may choke the UK’s pound-token market before launch

A House of Lords committee has told the Bank of England to rethink stablecoin caps before the UK’s regime is finalized.

The Financial Services Regulation Committee published its report, Stablecoins: waiting for regulation, on June 3, turning a technical debate over reserve design into a test of whether the UK can build a pound-denominated stablecoin market without making it uneconomic from the start.

The pressure point is the design of the safeguards. The committee supports 1:1 backing and accepts that stablecoins can create risks around financial stability, consumer protection, and illicit finance.

Its challenge is more specific: the Bank’s proposed safeguards may be calibrated for a market that does not yet exist in the UK.

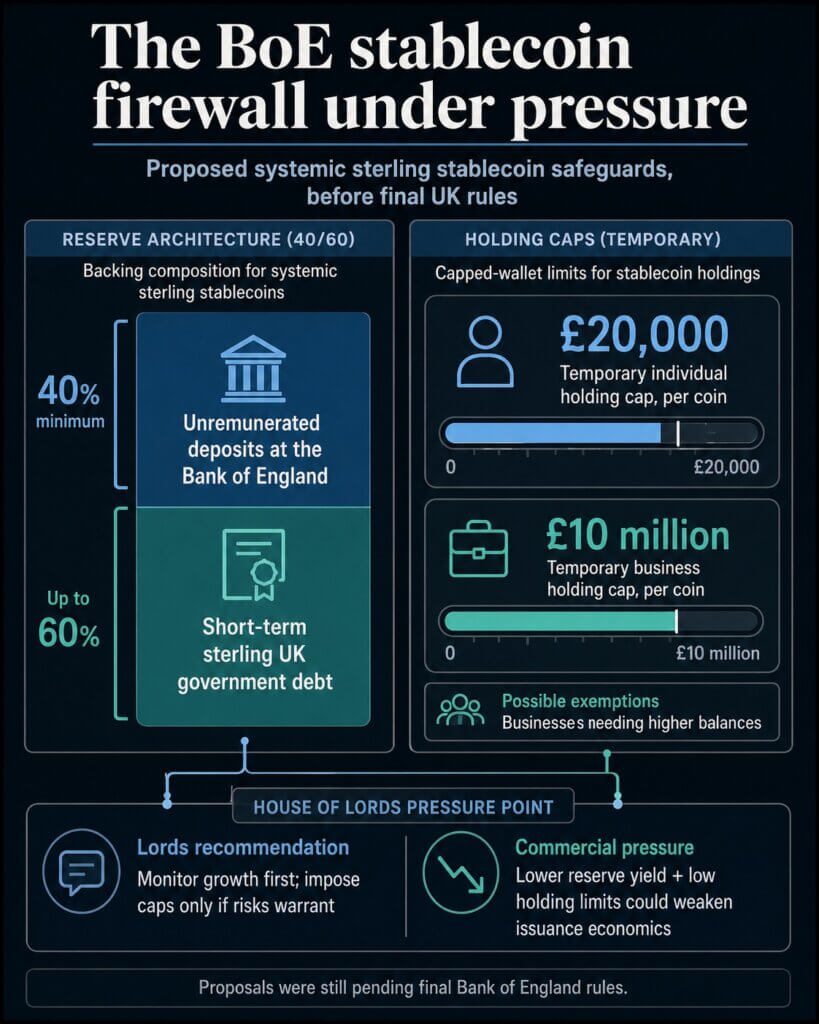

Two measures sit at the center of that critique. The Bank has proposed temporary per-coin holding limits of £20,000 for individuals and £10 million for businesses.

It has also proposed requiring systemic sterling stablecoin issuers to keep at least 40% of backing assets as deposits at the Bank of England that do not earn interest.

The Lords report says those choices could shape whether a GBP stablecoin market develops at all. If a pound stablecoin cannot be held in useful amounts or generate enough reserve income to support the issuer’s business, the UK could end up with clear rules, but few firms willing to build the products those rules are meant to govern.

The Rules Under Pressure

The Bank of England’s November 2025 consultation proposed a split backing model for systemic sterling stablecoins.

At least 40% of backing assets would sit as deposits at the Bank, while up to 60% could be held in short-term sterling-denominated UK government debt.

The Bank’s case is that central-bank deposits provide immediate liquidity if holders seek large redemptions in a short period. In its consultation, it said the threshold aligned with estimates of possible short-term redemption requests drawn from stress events in traditional and crypto markets.

The 60% government-debt allowance was meant to improve issuer viability compared with an earlier model that would have placed all backing assets in unremunerated central-bank deposits.

That compromise is now under pressure. The Lords committee concluded that remuneration and liquidity requirements for backing assets could have a significant effect on issuer viability and UK competitiveness.

It urged the Bank to consider the impact of requiring a proportion of unremunerated assets and to reconsider whether deposits held at the Bank should be remunerated at Bank Rate.

The committee also pushed the Bank toward a more flexible approach to backing-asset composition. It said the Bank should be open to a principles-based and less prescriptive model, with requirements adjusted as market behavior and risks become clearer.

The same logic applies to holding limits. The Bank’s proposal would cap each individual’s holdings of a systemic stablecoin at £20,000 per coin and each business’s holdings at £10 million, with possible exemptions for businesses that need higher balances in normal operations.

In a November news release, the Bank framed those limits as temporary tools to protect access to credit while the financial system adapts to new forms of money.

The committee’s recommendation was sharper. Given the early stage of the GBP stablecoin market, it said the Bank should monitor growth and impose holding limits only if financial stability risks clearly warrant them.

If limits become necessary, the committee said the Bank should consult to ensure they can be implemented in a practical way that still meets the Bank’s objectives.

Why The Bank Is Cautious

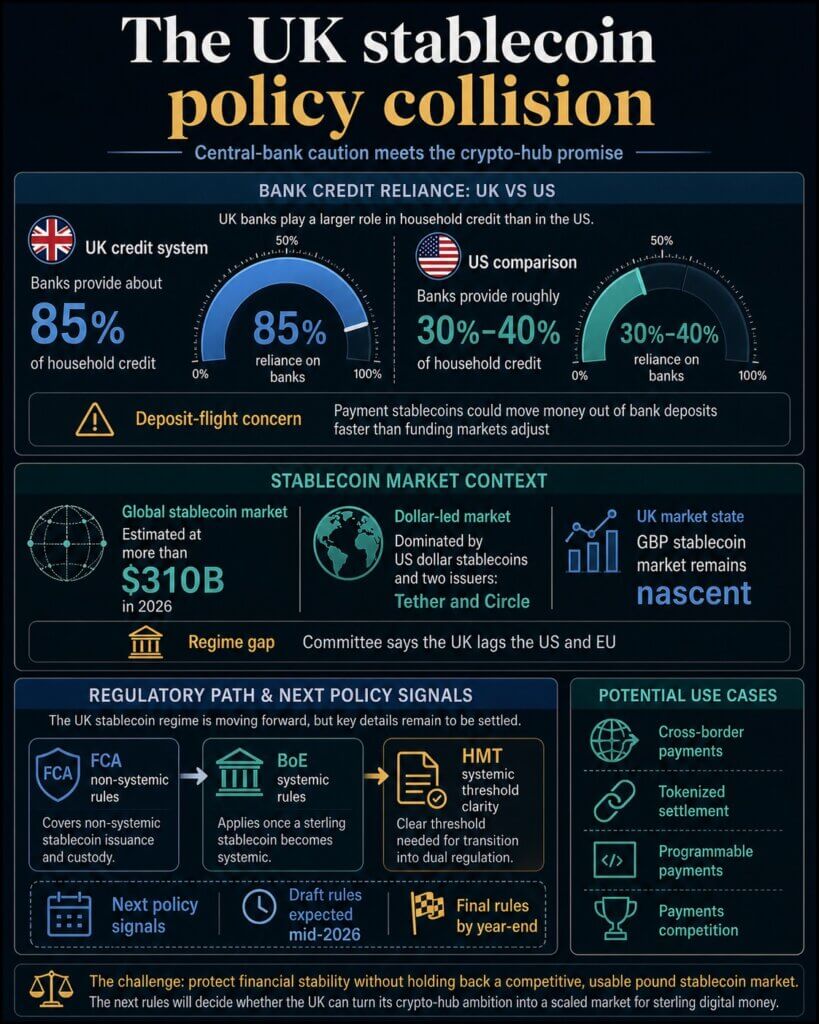

The Bank’s concern goes beyond competition with banks. In the UK, bank deposits do more work inside the credit system than they do in some other major markets.

In oral evidence to the committee in March, Sarah Breeden, the Bank’s deputy governor for financial stability, said banks provide about 85% of household credit in the UK, compared with roughly 30% to 40% in the US.

Her argument was that if deposits moved rapidly into payment stablecoins and that funding was not replaced, the result could be a drop in credit for households and businesses.

That is the financial-stability case for a circuit breaker. The Bank is designing for a future in which stablecoins are widely used as money for everyday payments, beyond their current use in crypto trading.

If adoption moved quickly through social media platforms, e-commerce networks, wallets, or automated payment tools, the Bank worries that money could leave deposits faster than banks and funding markets could adjust.

The committee accepts that risk. Its report says stablecoins can pose challenges around financial stability, illicit finance, and consumer protection.

It also welcomes 1:1 backing, audited reserves, disclosure, statutory trust protections, and the proposed Bank backstop lending facility for systemic issuers.

The disagreement is about timing and prescription. Lawmakers are asking whether the Bank should impose caps and reserve economics before there is enough evidence about how a pound stablecoin market would behave.

A protective rulebook could reduce the chance of a disorderly shift out of bank deposits. It could also make the regulated version of the product less attractive than offshore, dollar-denominated, or non-systemic alternatives.

The stakes are higher because the report describes the UK stablecoin market as nascent while the global market is already large and dollar-led.

It says the global stablecoin market was estimated at more than $310 billion in 2026, overwhelmingly dominated by US dollar stablecoins and two issuers, Tether and Circle.

For the UK, that creates a strategic problem. A sterling stablecoin market could support cross-border payments, tokenized settlement, programmable payments, and competition in payments.

It could also reduce the risk that UK users and businesses default to dollar stablecoins because pound alternatives never get enough regulatory clarity or commercial scale.

The committee says the UK is already lagging the US and EU in developing a stablecoin regime, though it says the country is now moving in the right direction.

The FCA’s stablecoin issuance and crypto custody consultation covers the non-systemic side of the regime, while the Bank’s rules apply once a sterling stablecoin becomes systemic.

The transition between those regimes remains one of the areas issuers need to understand before they can build durable business plans.

The Next Signal Is The Draft Rulebook

The timing makes the Lords report more than a retrospective critique. Breeden told the committee in March that the Bank expected draft rules in the middle of 2026, final rules by year-end, and applications from stablecoin issuers by the end of the year.

That means the next policy document will show whether the Bank treats the report as a reason to change the design or as a challenge to explain the existing model more clearly.

The signals to watch are specific: whether per-holder caps remain, whether the Bank shifts toward aggregate issuance guardrails or monitoring triggers, whether the 40% deposit share is adjusted, and whether any Bank deposits receive remuneration.

Rewards will count, too. The committee noted relatively little demand for issuers to pay interest on stablecoins, but said the treatment of rewards, rebates, or other incentives could affect the creation of a GBP stablecoin market and the UK’s international competitiveness.

That question connects stablecoin rules to the broader payments market, where card networks and financial apps already compete through reward structures.

The report also asks for more clarity from HM Treasury on when a stablecoin becomes systemic. That threshold is central for issuers because it determines when a firm moves from the FCA-only track into dual regulation by the Bank and FCA.

If the transition is too uncertain, scaling may become a risk in itself.

CryptoSlate has already covered adjacent UK payment infrastructure moves, including Revolut’s pound stablecoin sandbox trial and the Bank’s 24/7 settlement plans.

The Lords report moves the debate to a different point: whether the UK’s stablecoin rulebook will let a sterling market become commercially meaningful once tokenized payments enter the system.

The Bank is still finalizing the regime, and the committee is still asking for financial-stability protections. The new pressure is for the Bank to show that its safeguards will not stop a pound stablecoin market before it has a chance to form.

That is the live test for the UK’s crypto-hub promise. The next draft rules will show whether the Bank’s stablecoin firewall is a temporary guardrail, a redesign in progress, or a cost issuers decide the pound market cannot absorb.

Credit: Source link