SEC could start writing crypto rules before the Senate votes on CLARITY

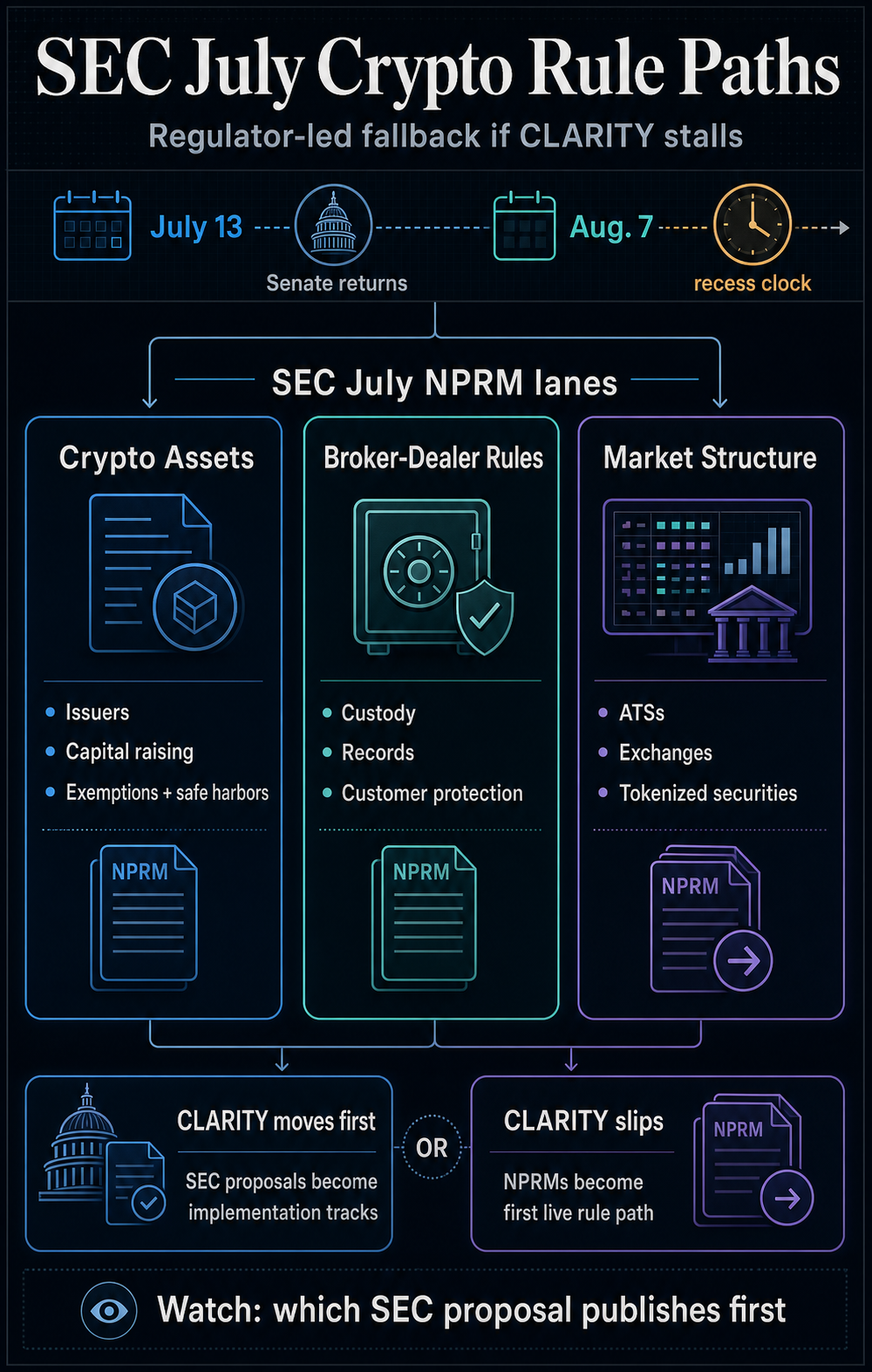

Three SEC crypto proposals are now penciled in for July, covering token offerings, broker-dealer custody and trading venues. The agency could start writing the rules before the Senate even decides whether to take up the CLARITY Act.

Earlier this week, SEC Chair Paul Atkins said the agency’s 2026 regulatory agenda aims to bring more crypto products onshore, create clearer rules for capital raising with crypto assets, and clarify how market participants can custody and facilitate the trading of tokenized securities on-chain.

According to him:

“[These efforts are to] ensure that the next chapter of financial leadership is written in the US, and that our capital markets continue to lead the world – in their depth, their dynamism, and their unrivaled ability to transform ingenuity into prosperity.”

That posture has translated into three July NPRM targets covering crypto-asset offerings, broker-dealer rules, and crypto market-structure amendments.

If any of those proposals is published this month, the SEC would move the crypto debate from policy signaling into a formal rulemaking process.

That would come as US lawmakers have yet to decide whether to bring the highly anticipated CLARITY Act to the Senate floor. The bill is designed to establish a federal framework for the crypto industry and clarify how oversight is split between the SEC and the Commodity Futures Trading Commission.

While CLARITY remains the broader market-structure vehicle, its momentum has slowed as the Senate calendar narrows.

The SEC’s July agenda puts the agency and Congress on competing tracks. CLARITY would address the broader question of who regulates what, while the SEC can move sooner on issuers, broker-dealers, exchanges and tokenized securities.

SEC’s July agenda targets crypto’s issuance-to-trading pipeline

The SEC has a chance to turn its July agenda into actual policy by starting rulemaking where crypto most often collides with securities law: how tokens are issued, how broker-dealers can custody them, and where they can be traded.

RegInfo’s July target puts crypto fundraising first, with the SEC’s Division of Corporation Finance weighing new rules for how digital assets can be offered and sold.

The entry says those rules could include exemptions and safe harbors designed to clarify the regulatory framework, provide greater market certainty, facilitate capital formation and protect investors.

That would put token issuers and projects seeking registration, exemption or disclosure paths near the front of the agency’s process. It would also move one of the industry’s longest-running disputes into a formal rulemaking channel after years in which crypto firms argued that the SEC relied too heavily on enforcement actions.

This is also the most legally sensitive of the three July entries. RegInfo lists the legal authority for the Crypto Assets proposal as “not yet determined,” meaning the agency has not identified the statutory footing in the agenda entry itself.

That does not preclude a proposal, but it could become a point of attack if the SEC tries to build a broad offering framework before Congress provides it with clearer authority.

Custody and broker-dealer compliance come next. A separate July entry covers possible amendments to financial responsibility, customer protection, recordkeeping, and reporting rules as they apply to crypto assets. The entry cites Rules 15c3-1 and 15c3-3, as well as Rules 17a-3 and 17a-4.

Those rules would shape how far regulated securities firms can go in crypto. Broker-dealers need clear treatment on capital, custody, customer protection, and books and records before they can support tokenized securities or crypto-linked products across regulated platforms.

Without that treatment, Wall Street firms may have demand for crypto products but still lack the compliance path to handle them at scale.

The SEC’s third target covers market structure, with possible Exchange Act changes governing crypto trading on alternative trading systems and national securities exchanges.

Together, the three July targets show the SEC is not only looking at one crypto issue in isolation. The agency is preparing possible rule paths across issuance, custody, and trading, which is the same sequence that any regulated crypto market would need to function.

A published SEC proposal would raise pressure on Congress

The race now turns on whether the SEC can put a crypto proposal into the Federal Register before Congress gives CLARITY a Senate vote.

If the SEC publishes one of its July proposals first, the agency would give issuers, broker-dealers and trading venues a concrete rulemaking process to respond to while the broader market-structure bill remains unresolved.

The debate would shift from Capitol Hill into SEC rulemaking, giving industry groups a chance to argue for broader exemptions and more workable custody and trading rules.

It could also change the legislative calculation. A live SEC proposal may give lawmakers a baseline to accept, narrow or override. It could also increase pressure on Senate leaders to act if lawmakers believe the agency is filling gaps that should be settled by statute.

Still, publication alone would not make the SEC path decisive. The proposals would need commission approval, public comment and possible revisions before becoming final. They could also face legal challenges or be reshaped by any market-structure bill Congress passes later.

That makes the July agenda important because of when it could start, not because of what it can finish on its own. It does not replace CLARITY or settle the full US crypto rulebook. But it gives the SEC a way to begin writing securities-side rules before the Senate decides whether the broader bill gets floor time.

The next signal is twofold: whether Senate leaders find time for the CLARITY Act before the Aug. 7 recess, and which SEC proposal is published first.

If Congress acts first, the SEC’s July agenda could set the machinery of a broader law in motion.

If the Senate stalls, the agency may start writing crypto’s securities rules before lawmakers vote.

Credit: Source link